This week the Federal Reserve released its Beige Book, which is a compilation of economic surveys taken through the better part of March till April 4th. According to the report, the economy improved in all 12 Federal Reserve districts. A sign that stimulus provided by current monetary policy, such as QE2, is having the desired positive impact.

Gains in manufacturing activity were expressed by every district, while modest increases in consumer spending were seen in a majority of districts.

The survey’s results were basically in-line with economic reports released the past week, showing growth for the month of March.

Industrial production in the U.S. grew by 0.8 percent in March, while capacity utilization increased to 77.4 percent. Retail sales rose 0.4 percent in March, generally in-line with economists’ expectations.

The above are good items for the economy and certainly represent a trend I hope continues. More economic activity means more jobs and less unemployed Americans, which is the Fed’s main motivation for current monetary policy.

The flipside of this coin is the rising price pressures that have continued to build through the first quarter of 2011. As discussed in the last letter, the Fed’s QE2 (second round of quantitative easing) is an act of currency devaluation.

The unintended effect of this policy is the additional pressure added to prices for basic materials (commodities), which is eventually past onto consumers as goods. We as consumers have thus far been insulated from this phenomena, with the glaring exception of oil & gasoline (I’m afraid to visit the gas station these days).

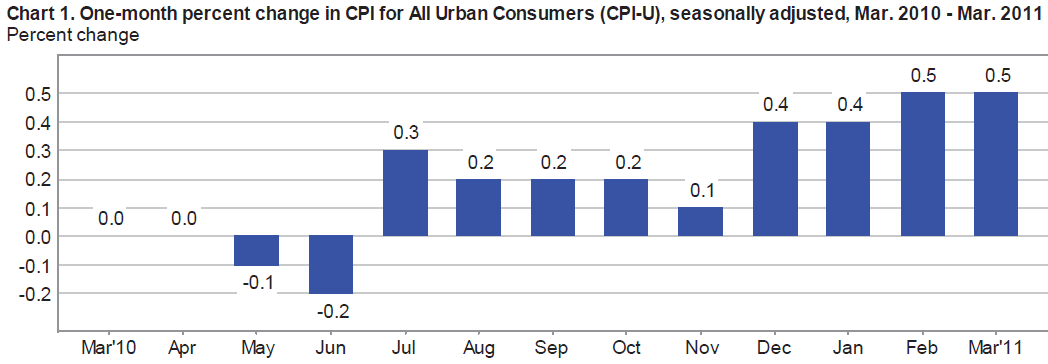

The below chart shows an aggressively increasing Consumer Price Index (CPI); a large chunk of the recent increases are due to the rise in oil, the second largest driver is the rise in food costs.

Retailers have done their best to minimize the costs they pass to the consumer in fear of losing business with the economy, and American consumer for that matter, still in a the recovery phase of the economic cycle. However, this will not last much longer as large brand-name manufacturers, such as Colgate and Procter & Gamble announced 5 to 7 percent price increases in recent weeks. These increases will likely get passed down to us, the consumer, at retailers such as Wal-Mart and Target.

In fact, Wal-Mart CEO Bill Simon recently stated that “Inflation is going to be serious. We are seeing cost increases starting to come through at a pretty rapid rate.”

Now, an environment of rising prices isn’t always a bad thing. Generally when you have increased economic activity and accelerating spending the price of items rise, it’s simple supply and demand.

The issue IS that average workers wages are not rising! The Bureau of Labor Statistics reported earlier in the month that hourly earnings in the U.S. were flat in March, though a 0.2 percent rise was expected. Wages were flat in February as well.

This compares to a 0.5 percent rise in the CPI for February and March. This divergence cannot become a long-term trend as our earnings will buy us less goods, weighing on consumer spending, the main driver of the U.S. economy.

The good news is based on the Fed’s comments Wall Street expects QE2 to end in June as planned. I have previously mentioned that we will likely see a nice pop in the US dollar in the months following the program’s end. This will reduce the cost of our imports, such as oil, and help relieve some price pressures for us.

As for a third round of quantitative easing, most economists I follow seem to think there is little likelihood it will occur until later in the year if the economy starts to falter.

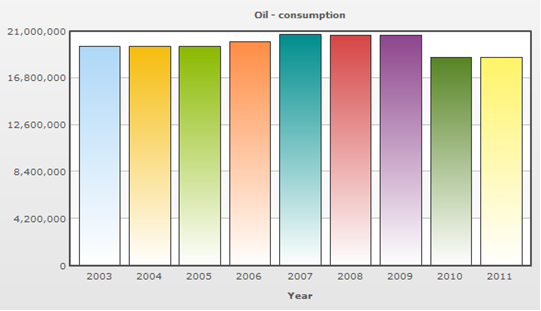

This notion becomes a bit more clear when you consider that increasing prices are supposed to be caused by increased demand, meaning too many dollars chasing too few goods. The problem with that equation here is that U.S. Oil demand has not increased. The accompanying chart shows that average demand actually fell in 2010 and is flat thus far in 20011. Yet the cost for all energy related goods, such as gasoline and heating oil, has increased.

This notion becomes a bit more clear when you consider that increasing prices are supposed to be caused by increased demand, meaning too many dollars chasing too few goods. The problem with that equation here is that U.S. Oil demand has not increased. The accompanying chart shows that average demand actually fell in 2010 and is flat thus far in 20011. Yet the cost for all energy related goods, such as gasoline and heating oil, has increased.